When moving to the US, your financial strategy will change because the way salary structures are computed is different. If you're wondering how to calculate your take-home salary once you start earning in dollars, you've come to the right place.

Before we list out ways to calculate your take-home salary, here are a few terms that you will need to know:

Gross Pay of your US take-home salary

Gross pay is the total amount (the salary in your joining contract) before any deductibles like income tax, insurance deductions, and allowances are applied. It is essential to know this amount because decisions like which tax bracket you fall in, the appraisal amount you are entitled to, etc., will be decided based on this amount.

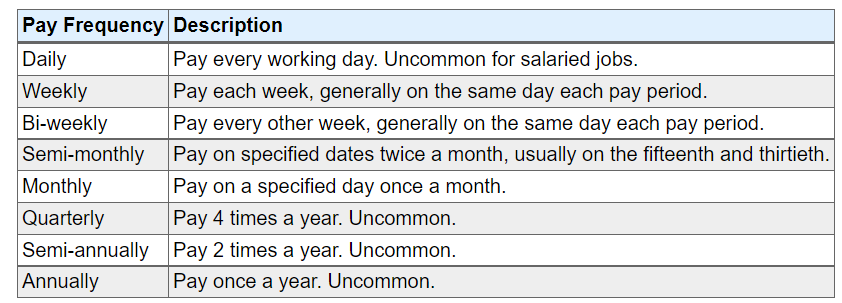

Pay Frequency of your US take-home salary

The pay frequency in the US differs from employer to employer. Common pay frequencies are:

One important distinction to note is the difference between bi-weekly and semi-monthly. Bi-weekly is every other week and this frequency generates two more paychecks a year compared to semi-monthly (26 paychecks compared to 24).

File Status

The IRS uses the following as your file status to calculate tax amounts:

Once you know which category you fall in, it will help you calculate your take-home salary.

Deductions

Deductions are expenditures that reduce your income and reduce the amount of tax you have to pay (by reducing the taxable amount). Deductions fall into three main categories:

Pre-tax deductions withheld

These are deductions that are deducted directly by the employer before paying the employee their salary. Deductions like retirement savings (401K), health insurance premiums, child support payments, etc., fall into this category.

Deductions not withheld in your US take-home salary

These are deductions that are not directly deducted by the employer but can be subtracted from the total taxable income. These deductions include student loan interests, IRA contributions, tuition, etc.

Itemized deductions

Any expenditure made on products, services, or contributions that are eligible for tax relief can be subtracted from the taxable income. These include costs like qualified mortgage interest, charitable donations, medical/dental expenses, etc.

If you do not use itemized deductions, you can apply the standard deduction - $12,550 for single households and $25,100 for married couples filing jointly for the tax year.

Income Tax

Federal income tax

Levied by the US federal government, this amount is levied by the IRS (Internal Revenue Service) and is generally the most significant portion you pay in taxes. The percentage you pay depends on which tax bracket you fall in.

State income tax

Like federal income tax, the state income tax is levied by the state towards the general development and improvement of the community. Not all states in the US charge state income tax.

Locality/City/Municipal income tax

Some municipalities (a very small number) impose this tax which can be deducted from the federal income tax if itemized.

FICA Tax

Social Security tax and Medicare tax together form the FICA Tax. Social security provides monetary funds and benefits to retired, unemployed, or disabled people, and the federal government collects this amount from society.

Take-Home Pay

Once you have the above information in hand, you can calculate your take-home salary. The easiest way to do that is to use a take-home salary calculator. Some ways to increase your take salary are re-evaluating payroll deductions (opt for lower insurance, for example), opening a flexible spending account, or temporarily pausing your 401K (in case of a financial emergency).

A headstart to life in the U.S.

Zolve allows you to apply for a U.S. Bank Account and high limit Credit Card from your home country itself; no SSN is required. As a working professional, you can get a credit limit of up to $10,000.

Disclaimer: The products, services, and offerings mentioned in this blog are subject to change and may vary over time. We recommend visiting our official website for the most up-to-date information on Zolve's offerings.